Constant Consumption vs. Constant Scrap in AX 2012 and How it Affects Cost

When using formulas in AX 2012 there are two main options for accounting for a fixed usage of material: constant consumption or constant scrap. We'll explore both options and how it affects cost in this post. The reasons for that fixed usage could be that there is start-up for the process or a known amount of waste, due to not being able to get everything out of a mixing vessel for example. Deciding which option would be preferred for your organization could depend on the preference of accounting and where you want see that cost in a standard cost environment.

Using Constant Scrap

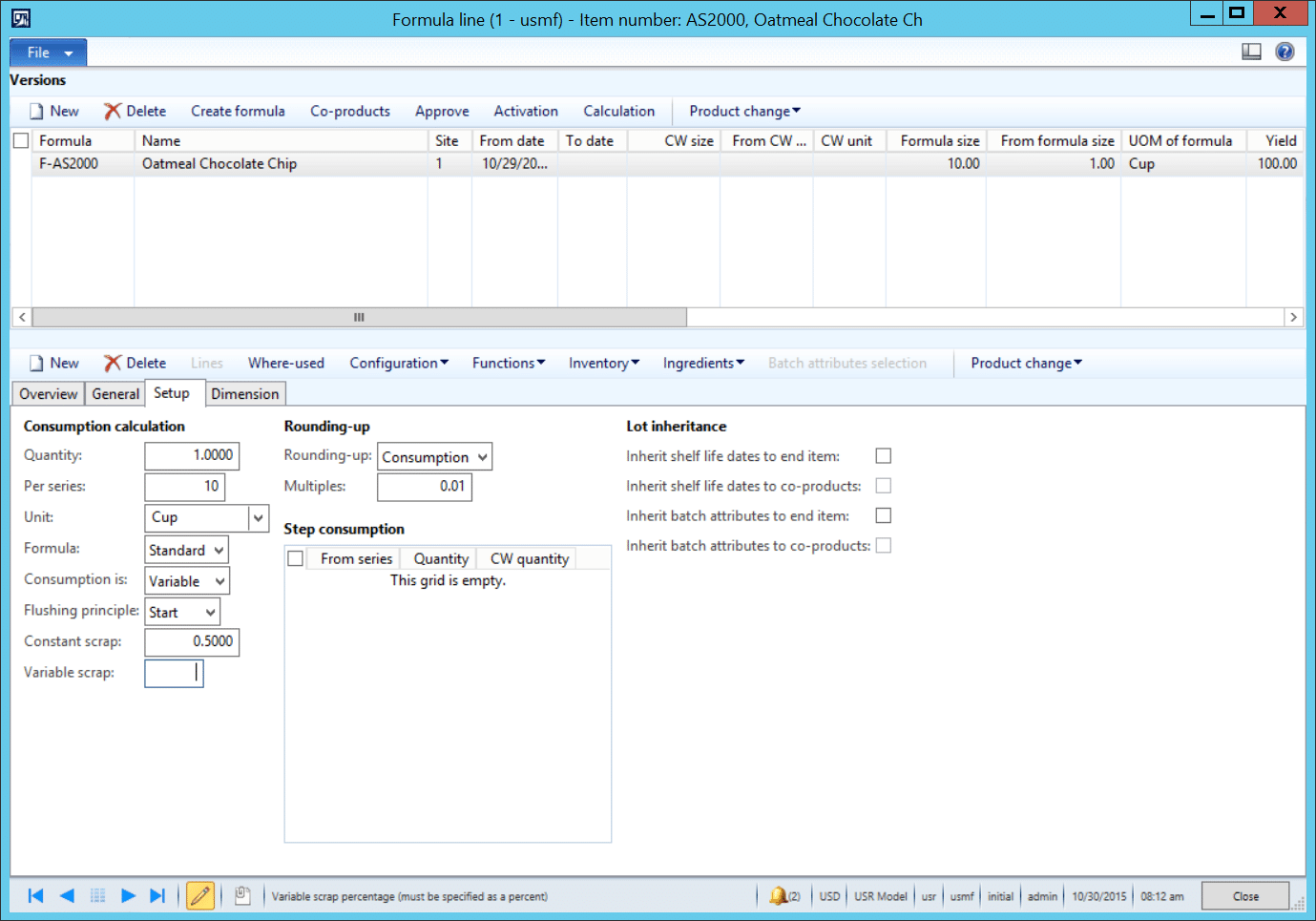

On the formula in the setup tab there is a field for constant scrap. In this field you would enter an amount of material that gets consumed in the process, generally as waste, that is fixed no matter the batch size.

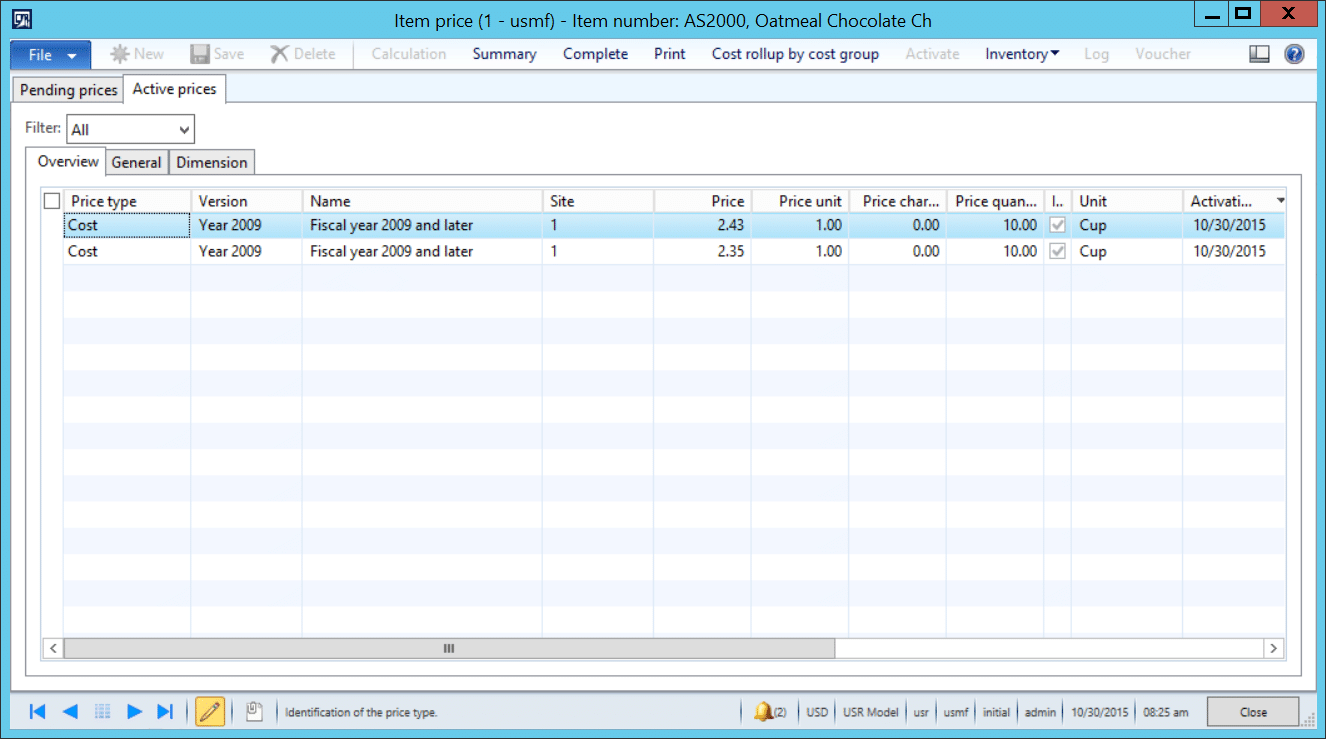

When the fixed quantity is placed in the constant scrap field and the calculation functionality is used to generate the item price, the value of the constant scrap is included in the price field. In the example below, the cost on the bottom is calculated without any constant consumption. The price on the top is calculated with a constant scrap on one of the lines.

The advantage of using the constant scrap field is that it is less work for the person setting up the formula and all of your cost price is in one field.

Using 'Consumption is Constant' Line

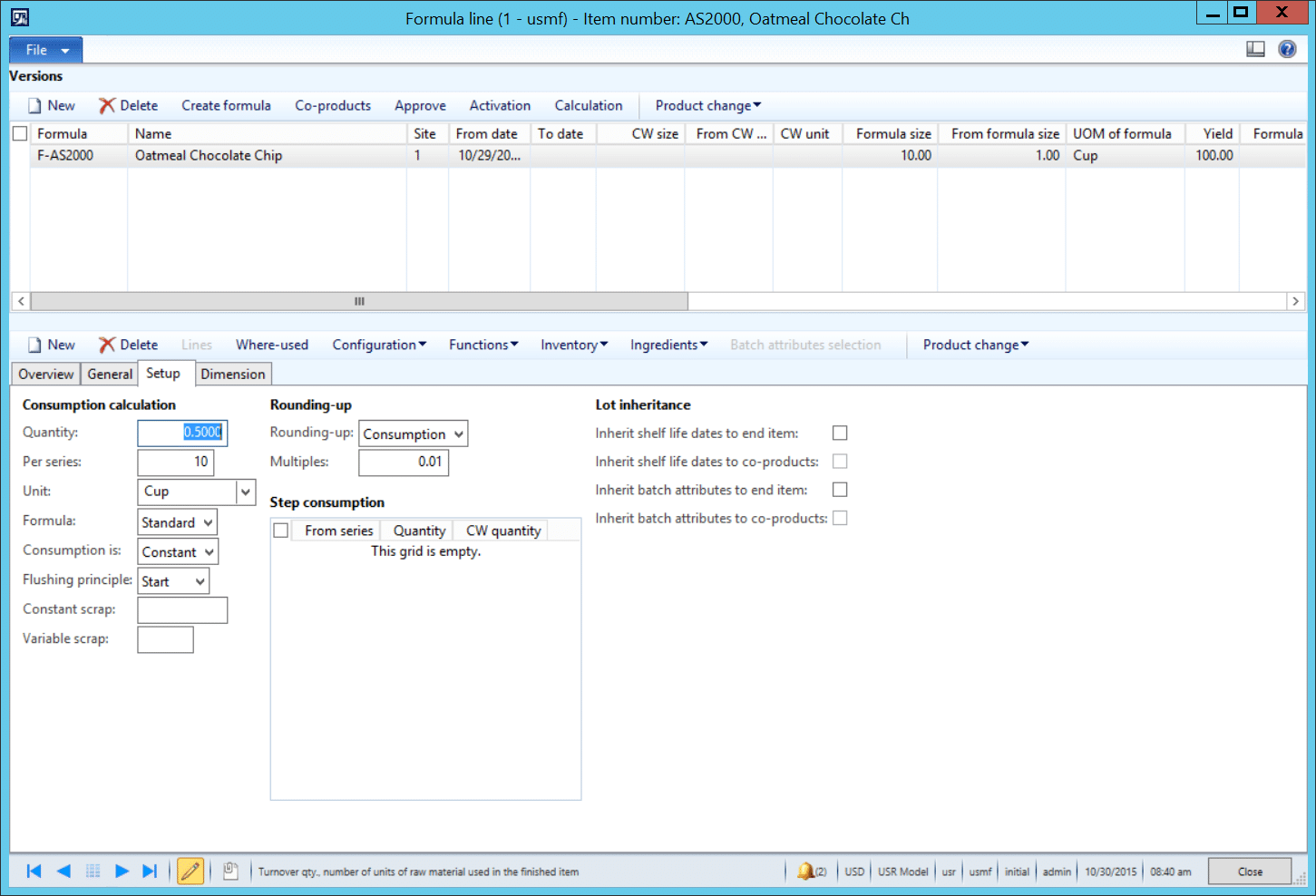

Another way to handle fixed consumption would be to change the 'consumption is' field from variable to constant. This is also done in the setup tab of the formula lines. Now instead of putting your quantity in the constant scrap field, the quantity would go in the quantity field. Again, with the 'consumption is' field set to constant, the value in the quantity field is fixed no matter the batch size.

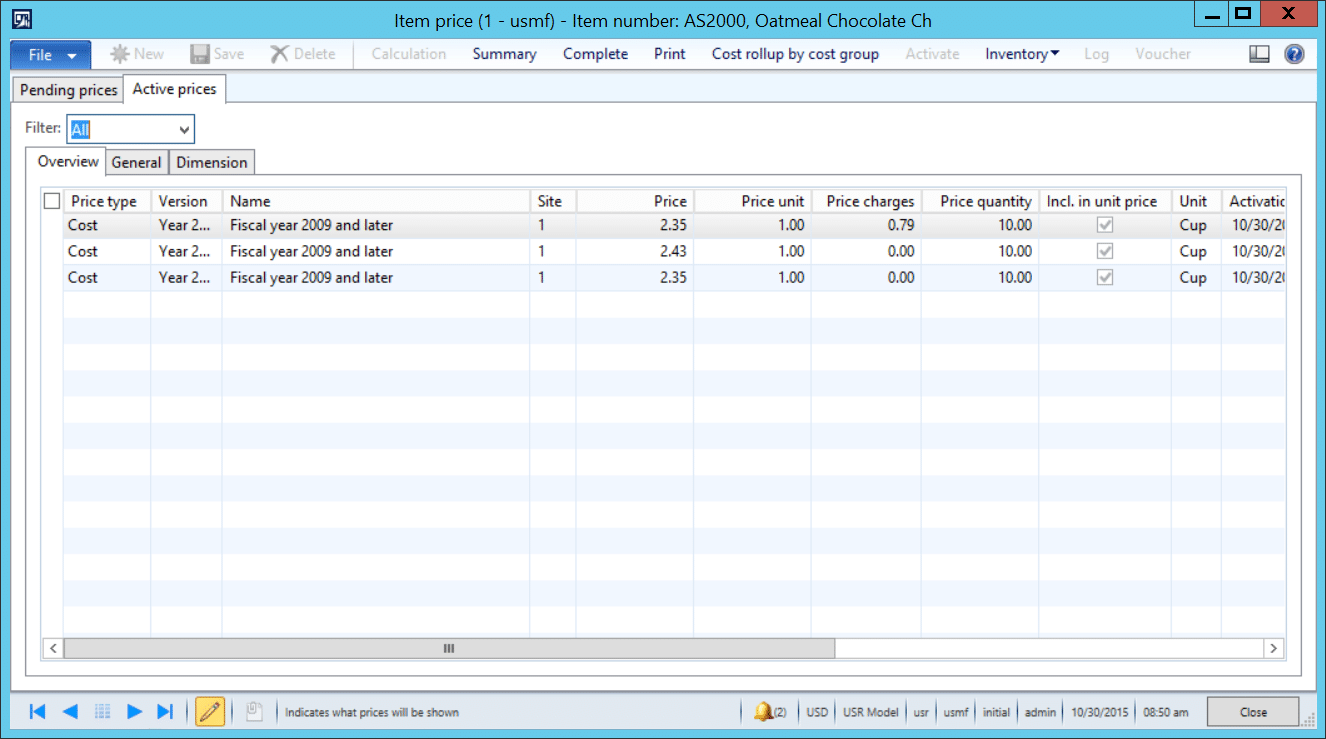

When the fixed quantity is placed on a separate line with the 'consumption is' field set to constant, and the calculation functionality is used to generate the item price, the value of the fixed quantity is included in the price charges field. In the example below, the cost on the bottom is calculated without any constant consumption. The price in the middle is calculated with a constant scrap on one of the lines. And the price on the top is calculated with the fixed quantity on a separate line. In this case the price charges amount is divided by the price quantity, so the per part affect is $0.08 just like it was when using the constant scrap field.

The advantages of creating a separate line with the consumption is set to constant is that those fixed quantity costs are broken out separately. This would allow a business to focus on items with a large price charges value as areas of process improvement to try and reduce that quantity. The disadvantage is that it is more work for the person setting up the formula.

Constant Consumption vs. Constant Scrap Summary

In the end, the method chosen is largely dependent on the needs and the preference of the business. Both methods result in the same per unit cost, but the amount of work required and the ability to have those costs broken out or not are the deciding factors.

Under the terms of this license, you are authorized to share and redistribute the content across various mediums, subject to adherence to the specified conditions: you must provide proper attribution to Stoneridge as the original creator in a manner that does not imply their endorsement of your use, the material is to be utilized solely for non-commercial purposes, and alterations, modifications, or derivative works based on the original material are strictly prohibited.

Responsibility rests with the licensee to ensure that their use of the material does not violate any other rights.