Periodic vs. Perpetual Inventory: Mark-to-Market Accounting in Dynamics 365 and Levridge

Managing commodity inventory requires more than tracking quantities and costs. For many agribusinesses, inventory must also be valued at market value for month-end financial reporting. That creates an important accounting consideration: how should mark-to-market (MTM) adjustments be handled when inventory is managed using a periodic or perpetual inventory method? This topic is especially relevant for commodity processors, grain businesses, ag retailers, and other agribusinesses that need to account for commodity inventory at market value.

In Dynamics 365 Finance and Operations, paired with the Levridge agribusiness solution, organizations can manage industry-specific commodity accounting needs, including board price, basis, inventory quantity tracking, and mark-to-market valuation. Levridge includes functionality to calculate the market value of inventory on hand and, with the right configuration, automatically posts the mark-to-market journal entry.

The accounting impact of that journal entry depends on the inventory method your business uses. If you use periodic inventory, the automated mark-to-market entry can be used to value inventory at month end. If you use perpetual inventory, additional steps are needed to avoid overstating inventory by posting market value on top of the existing inventory value.

This article walks through examples of both periodic and perpetual inventory methods and explains how the mark-to-market journal entry impacts financial statements in each scenario.

Periodic Inventory Transactions & Mark to Market Adjustment

The following examples use a simplified commodity transaction scenario to show how mark-to-market valuation flows through the general ledger. While the transactions are simplified for illustration, the concepts apply to agribusinesses using Dynamics 365 Finance and Operations with Levridge to manage commodity purchases, sales, inventory quantities, and month-end market valuation.

In this scenario, under a periodic inventory method, inventory is not carried on the balance sheet during the month, so the mark-to-market entry establishes the month-end inventory value.

Facts:

*See Appendix A for required configurations in D365 F&O in order to set up a periodic inventory system for inventory with a mark to market (MTM) inventory valuation requirement.

- ABC Company buys commodities which must be valued at Market Value for month end financial statements.

- ABC uses a Periodic Inventory method. As such, inventory is valued at $0 throughout the month and no inventory transactions are posted to the General Ledger (GL).

Transactions:

*See Appendix C for the Menu Path in D354 F&O and Levridge transactions

- ABC Co. purchases 1000 Bushels (BU) of Commodity X during the month at a Board Price of $10.05 and a Basis of 0.25, for a Net Price of $10.30 per BU.

- ABC Co. sells 250 BU of Commodity X during the month at a Board Price of $10.10 and a Basis of $0.30, for a Net Price of $10.40 per BU.

- At Month End, ABC Co has 750 BU (1000 purchased less 250 sold) remaining on hand of Commodity X at a Market Value of $10.35.

Transaction Entries:

*Refer to Appendix A for Required D365 F&O and Levridge Configurations & Appendix B for details of where transactions are posted in D365.

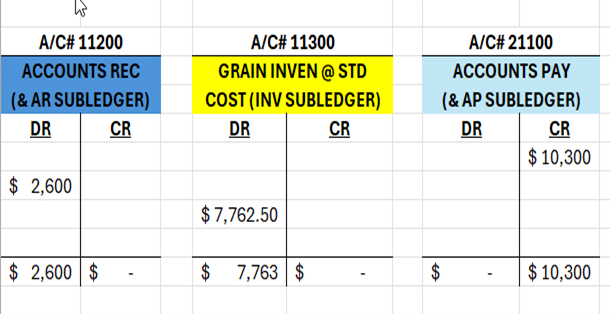

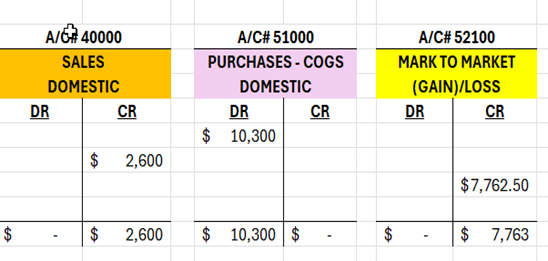

- Record the Purchase of Commodity X

DR PURCHASES $10,300 (1000 BU * $10.30 PURCH PRICE)

CR ACCTS PAYABLE ( 10,300) (1000 BU * $10.30 PURCH PRICE) - Record the Sale of Commodity X

DR ACCTS RECEIVABLE $ 2,600 (250 BU * $10.40 SALES PRICE)

CR SALES ( 2,600) (250 BU * $10.40 SALES PRICE) - At Month End, value Inventory at Mark to Market – Auto Posted by Levridge

DR INVENTORY $7,762.50 (750 BU * $10.35 MARKET PRICE)

CR MARK TO MKT GAIN/LOSS (7,762.50) (750 BU * $10.35 MARKET PRICE)

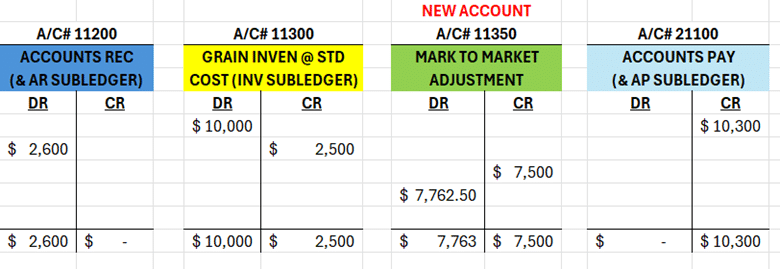

Summary of GL Activity in T-Account Form:

Balance Sheet Accounts:

P&L Accounts:

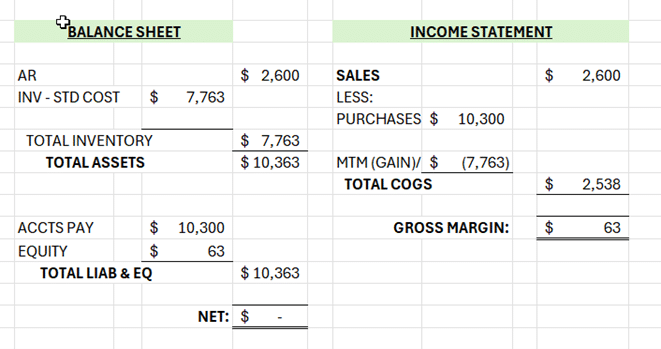

Summary Month End Financial Statements - Periodic Inventory:

As shown above, the periodic inventory method allows the business to track commodity inventory quantities throughout the month while keeping inventory value at $0 in the general ledger until month end. With Levridge, the mark-to-market calculation can then be used to post the market value of inventory on hand and properly reflect commodity inventory value for financial reporting.

Perpetual Inventory Transactions & Mark to Market Adjustment

For organizations using perpetual inventory, the month-end process requires a different approach. Because inventory value is already being recorded throughout the month using FIFO or standard cost, posting the full Levridge mark-to-market journal entry directly to the same inventory account could duplicate inventory value. The goal is to preserve the integrity of the perpetual inventory subledger while still reporting inventory at market value for month-end financial statements. So, what is the best way to handle the Mark to Market (MTM) adjustment journal under a perpetual inventory costing method?

Below is a set example of Perpetual Inventory Transactions (using Standard Cost). These examples show how perpetual inventory can provide more timely visibility into inventory value and gross margin throughout the month, while still allowing the organization to make the appropriate mark-to-market adjustment at month end. This can be done by adding some MTM inventory accounts to your chart of accounts and making a monthly reversing entry to zero out your perpetual inventory (prior to posting the Mark to Market Adjustment).

In this scenario, inventory is already carried on the balance sheet, so the process must remove the perpetual value before recording the market value adjustment.

Facts:

*Refer to Appendix B for required configurations in D365 F&O in order to set up a periodic inventory system for inventory with a mark to market (MTM) inventory valuation requirement.

- ABC Company buys commodities which must be valued at Market Value for month end financial statements.

- Throughout the month, ABC values their commodities at a Standard Cost.

- Commodity X has a Standard Cost of $10.00 per Bushel (BU).

Transactions:

*See Appendix D for the Menu Path in D354 F&O and Levridge transactions

Appendix D:

APPENDIX-D-MANAGING-THE-MARK-TO-MARKET-ADJUSTMENT-IN-D365-FO-LEVRIDGE-TRANSACTIONS-–-PERPETUAL-INVENTORY.pdf

- ABC Co. purchases 1000 BU of Commodity X during the month at a Board Price of $10.05 and a Basis of 0.25, for a Net Price of $10.30 per BU.

- ABC Co. sells 250 BU of Commodity X during the month at a Board Price of $10.10 and a Basis of $0.30, for a Net Price of $10.40 per BU.

- At Month End, ABC Co has 750 BU (1000 purchased less 250 sold) remaining on hand of Commodity X at a Market Value of $10.35.

Transaction Entries:

*Refer to Appendix B for Required D365 F&O and Levridge Configurations & Appendix D for details of where transactions are posted in D365.

- Record the Purchase of Commodity X

DR INVENTORY $10,000 (1000 BU * $10.00 STD COST)

CR ACCTS PAYABLE ( 10,300) (1000 BU * $10.30 PURCH PRICE)

DR PURCH PRICE VAR 300 (DIFFERENCE) - Record the Sale of Commodity X

DR ACCTS RECEIVABLE $ 2,600 (250 BU * $10.40 SALES PRICE)

CR SALES ( 2,600) (250 BU * $10.40 SALES PRICE)

DR COST OF GOODS SOLD $2,500 (250 BU * $10.00 STD COST)

CR INVENTORY $2,500 (250 BU * $10.00 STD COST)

3. At Month End, value Inventory at Mark to Market

Create a Reversing Entry to Bring Perpetual Value to zero. (Utilize a Mark to Market Adjustment Acct on the Balance Sheet to maintain the integrity of the Perpetual Inventory account value, which reconciles to the inventory subsidiary leger.)

DR MARK TO MKT ADJ GAIN/LOSS $7,500.00 (750 BU * $10.00 STD COST)

CR MARK TO MKT ADJ BAL SHT (7,500.00) (750 BU * $10.00 STD COST)

Mark to Market Journal Entry, which is also a reversing entry, automatically posted by Levridge

DR MARK TO MKT ADJ BAL SHT $7,762.50 (750 BU * $10.35 MARKET PRICE)

CR MARK TO MKT GAIN/LOSS (7,762.50) (750 BU * $10.35 MARKET PRICE)

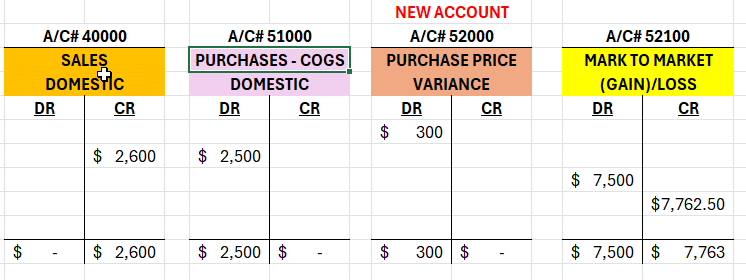

Summary of GL Activity in T-Account Form:

Balance Sheet Accounts:

P&L Accounts:

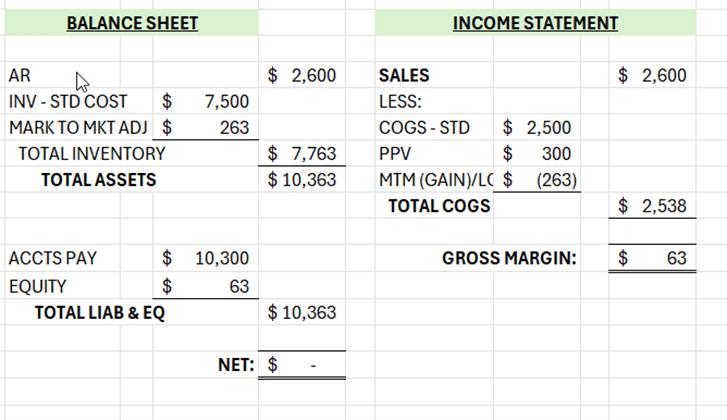

Summary Month End Financial Statements - Perpetual Inventory:

By using this method of entries for perpetual inventory, the end result is that the financial statements properly value inventory at Market Value of $10,363 (750 BU @ $10.35 Market Price).

In addition, the P&L reflects the same gross margin as periodic inventory; however, the perpetual inventory allows financials to potentially be reviewed throughout with a better estimate of expected result.

In the standard costing model above, the Mark to Market Gain reflects a $263 unrealized gain in inventory of 750 BU of Commodity X valued at $10.35 at month end compared to the $10.00 Std Cost. The PPV of $300 is the amount of price changes on purchases throughout the month. The Std COGS account recognizes the 250 BU sold at $10.00 Std Cost. Breaking out these items into their own accounts can assist in the month end analysis of gross margin.

Finding the Right Fit for Your Ag Business Inventory

Under the terms of this license, you are authorized to share and redistribute the content across various mediums, subject to adherence to the specified conditions: you must provide proper attribution to Stoneridge as the original creator in a manner that does not imply their endorsement of your use, the material is to be utilized solely for non-commercial purposes, and alterations, modifications, or derivative works based on the original material are strictly prohibited.

Responsibility rests with the licensee to ensure that their use of the material does not violate any other rights.