Fixed Price Projects and Recognition of Immediate Losses in Dynamics 365 Project Operations

Most companies will encounter a fixed price project that was either not estimated well or faced unforeseen challenges, resulting in an overall loss or negative margin, (with or without pending change orders.) In many cases, accounting rules require companies to recognize losses on fixed‑price projects as soon as a loss is anticipated, even if the project itself is still ongoing.

If your company’s requirements are to recognize losses as soon as a loss is projected, Microsoft Dynamics 365 Project Operations provides configuration options to support that approach.

This post uses two examples to illustrate how loss recognition works for fixed‑price projects using the cost‑to‑complete method, and how enabling foreseeable loss recognition affects revenue recognition and margin reporting when a project is forecasted to run at a loss.

Project Group Configuration and Shared Project Setup

Both examples share the same setup and assumptions outlined below.

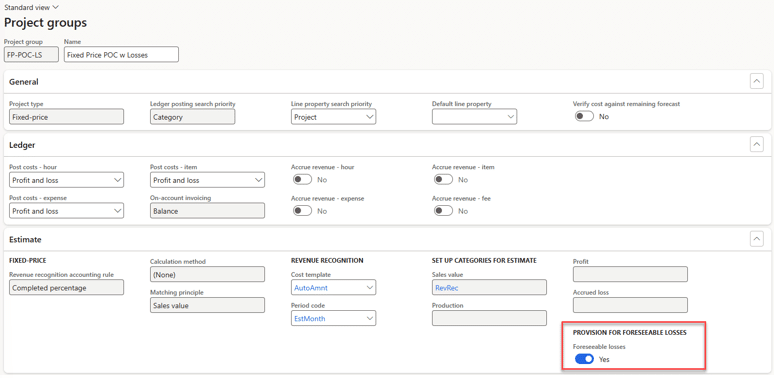

To support immediate loss recognition, be sure your project group has the option selected to record the provision for foreseeable losses. This allows a projected loss to be recorded as soon as it is identified.

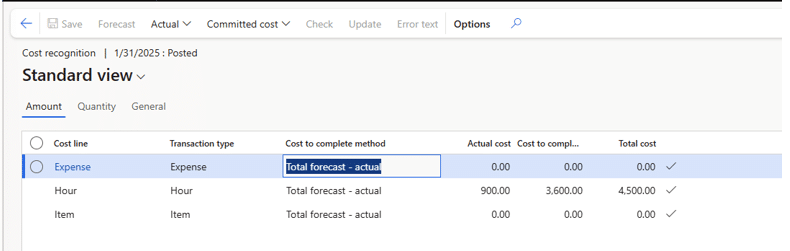

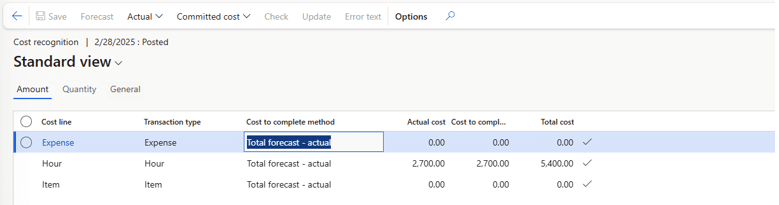

Note: the cost to complete method in this case is Total forecast - actual

Shared Project Assumptions and Initial Execution

At project creation:

- Forecast for 25 hours of Consulting at $180 per hour for total cost of $4,500

- Contract value a fixed $5,000

- Overall margin 10%

Month 1:

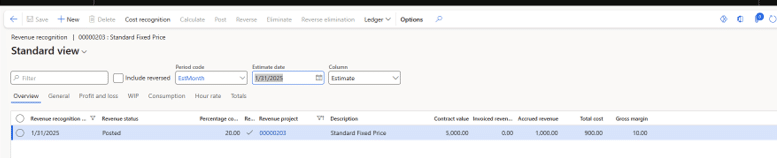

- Incurred 5 hours of Consulting at $180 per hour for total actual cost of $900

- Revenue recognized on both projects is identical

- [(Total actual cost / Total forecast cost) * Total Contract value] – sum of prior period revenue

- [($900/$4,500) * $5,000] - $0 = $1,000

Month 2:

- The project manager realizes the project forecast cost needs to be revised without a change order and this project will realize a net loss at the end of the project.

- Revising the forecast cost to 30 hours of consulting at $180 for a revised total cost forecast of $5,400, since the contract value did not change, the PM is forecasting a $400 overall loss on the project and a margin of -8%

- Actual hours recorded in month 2 were 10 hours at $180 for $1,800

Revenue Recognition Formula Varies in the Two Examples

Consider the following identical projects

- Example A uses the cost‑to‑complete method to calculate progress and revenue but does not recognize foreseeable losses

- Example B uses the same cost‑to‑complete method and project setup, but the project group is configured to recognize foreseeable losses when a loss is projected.

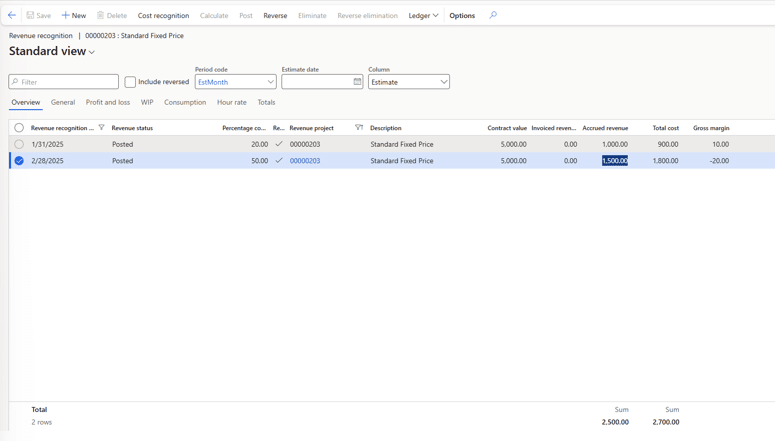

Example A: Revenue Recognition Without Foreseeable Losses

In this scenario, the project uses the cost‑to‑complete method to recognize revenue but does not recognize a projected loss until it is realized through ongoing project execution.

Formula:

[(Total actual cost / Total forecast cost) * Total Contract value] – sum of prior period revenue

[($2,700 / $5,400) * $5,000] - $1,000 = $1,500

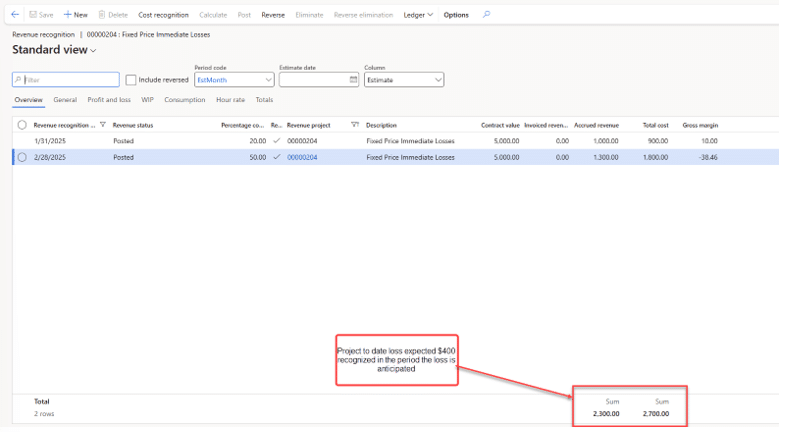

Example B: Revenue Recognition With Foreseeable Losses

Example B on the other hand has a slightly different formula to recognize the overall project loss in the period it is projected that the loss will occur (foreseeable losses):

When the project group is set to recognize foreseeable losses, the overall project to date dollar value loss will be recorded as the actual dollar value loss. In the above case the project-to-date loss will be the $400 projected overall loss recognized in Month 2 when the loss was projected.

Note: the project to date actual margin % is lower than the overall projected project margin % of -8%

-$400 / $2,300 = -17.4% margin

For subsequent periods, the total period revenue will equal total period actual cost leaving the project to date dollar value margin at $400 until the end of the project.

If the forecast is updated or the contract value changes, this would also update the overall dollar value margin and the revenue recognition results, however, the rules above would still be applied.

Final Considerations

It is important that the company’s project accounting leadership determine the best configuration for meeting the accounting rules for recognizing revenue within the project module. The approaches outlined in this blog are just a few of the several ways Dynamics 365 Project Operations can be configured to handle fixed‑price projects and recognize foreseeable losses.

Under the terms of this license, you are authorized to share and redistribute the content across various mediums, subject to adherence to the specified conditions: you must provide proper attribution to Stoneridge as the original creator in a manner that does not imply their endorsement of your use, the material is to be utilized solely for non-commercial purposes, and alterations, modifications, or derivative works based on the original material are strictly prohibited.

Responsibility rests with the licensee to ensure that their use of the material does not violate any other rights.