How to Compare Sales Receivables to Your GL Accounts in Microsoft Dynamics GP

At some point while using Microsoft Dynamics GP, you may notice your Accounts Receivable and General Ledger accounts don’t match your trial balance total. The best process to remedy this imbalance is to go through your records on a month by month basis and identify the month where there’s a discrepancy. Once you identify the month, drill into the transactions to discover where the error took place. One of the tools that will help is the ‘Reconcile to GL’ tool which will help you identify the transactions causing the issue.

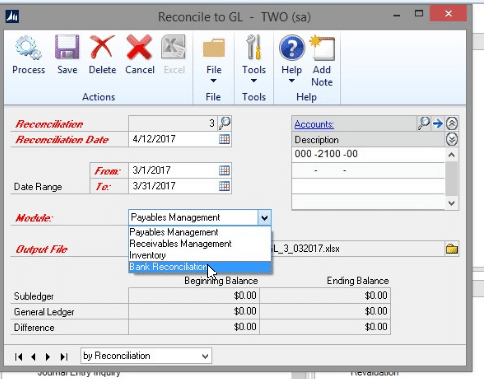

This tool allows you to choose if you want to reconcile several different modules including payables, receivables, inventory and bank rec.

You can then choose the date range you want to look at and it will identify those transactions that aren’t updated in one module or the other. When you export it, an excel file is generated that will help you compare both accounts.

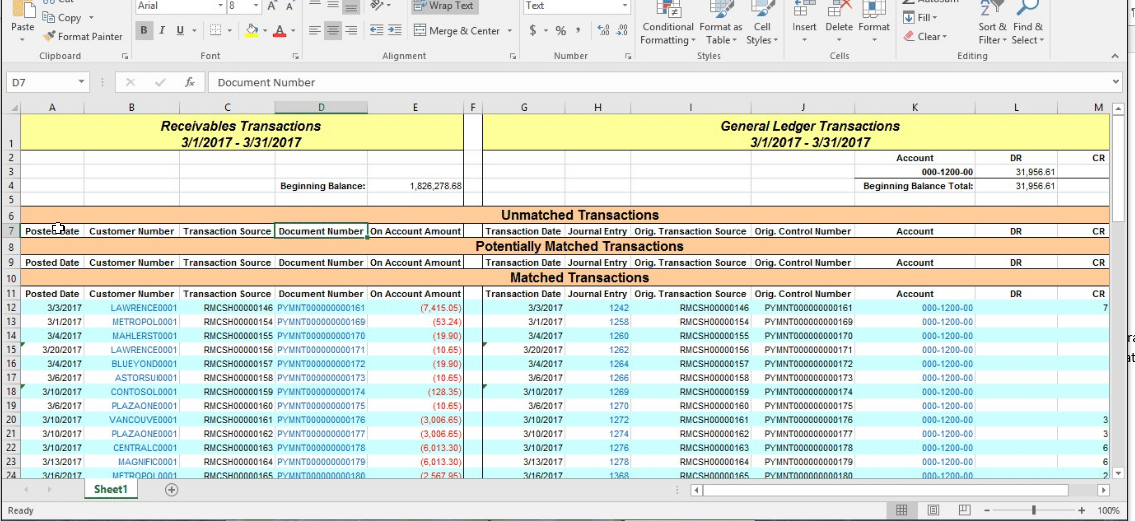

You can then compare your accounts and make sure everything is matching up dollar amount to dollar amount. The spreadsheet does link back to Microsoft Dynamics GP directly so if you click on a line item, it will take you to Microsoft Dynamics GP to see the transaction and details.

*Note: Please note that the beginning balances on the spreadsheet are unreliable. Only use these spreadsheets to compare transactions, NOT balances. Do not use this feature to compare balances.*

If you have any more questions about how to compare sales receivables to your GL accounts in Microsoft Dynamics GP, feel free to contact us at Stoneridge Software.

Under the terms of this license, you are authorized to share and redistribute the content across various mediums, subject to adherence to the specified conditions: you must provide proper attribution to Stoneridge as the original creator in a manner that does not imply their endorsement of your use, the material is to be utilized solely for non-commercial purposes, and alterations, modifications, or derivative works based on the original material are strictly prohibited.

Responsibility rests with the licensee to ensure that their use of the material does not violate any other rights.